What is a “Cash Balance” Pension Scheme?

A cash balance scheme is a type of pension defined benefit pension scheme, where the guarantee is a notional post, or cash balance. What this means is, your scheme will provide you with a pretend pot of cash that usually increases by inflation, or a fixed amount each year.

At the point you come to retire, there are a few choices you may have.

One of these options is to purchase an annuity, which the scheme will do. This will provide you with a lifetime income, and you may have some options to build into it. This could include a spouse’s pension, inflation proofing or a guarantee period. These features will have different implications for the level of income it will provide.

Some schemes may not be flexible, and the income would be prescriptive. So you may have to buy an annuity that is not quite right for your circumstances. As a single person, it is often costly to purchase a spouse’s pension as part of an annuity that has no benefit.

However some schemes we have seen in the past have conversion rates that they use to convert the cash balance into an income, though these are not fixed and can change. This does not apply to all of the cash balance plans, and some may use annuity providers on the market.

It is important to note that with a lot of cash balance schemes, there are hybrid benefits, so you may also have a defined contribution pension, which refers to an actual pot. This is not to be confused with the notional Cash Balance “pot”, which is a defined benefit.

One of the other possible options with a cash balance pot at retirement is taking the whole pot as a lump sum. This would mean 25% paid as tax free cash, and the rest subject to your marginal rate of tax. For people with large pensions, this could mean a large amount of the lump sum payment paid at 45% tax!

Taking a cash balance scheme as a one off lump sum would mean a lot of the pot would be lost in tax.

Cash Balance Pension Transfer

The other choice you have, which will apply to most cash balance scheme’s is a transfer out of the scheme. The scheme will often not give you the cash balance as the amount to be transferred, they will instead give you a (typically) smaller Cash Equivalent Transfer Value, or CETV.

This means you will give up the cash balance pot, that is likely to have inflation protections, and the ability to buy an annuity income, and in exchange take a smaller transfer value, to go to a new provider/pension scheme.

This avoids the large amount of tax payable, as the transfer value would still be inside the pension, and on transfer you have the option for investing the pension, keeping it invested, opt for flexi access drawdown to manage withdrawals or purchase an annuity.

Flexi-access drawdown will enable you to manage tax, and the annuity may offer something more suitable to your circumstances, than if a scheme is forcing you to buy a restrictive income.

But you may be reading this thinking…

Why would I take a smaller transfer value?

It is an excellent question! The main reason for doing so, is the transfer value can be invested and would act as an actual pot going up by investment returns, whereas the cash balance (notional pot), would only go up by inflation, typically with a cap.

To a large extent, when your transfer value is calculated, this inflation vs investment growth is already considered, so it is of little relevance. The actuaries for your scheme will try to work out what the cash balance at retirement would be, and “discount it back”.

For example, if they think that at retirement age, the cash balance will be £100,000, they will look at that and calculate the amount needed today, to invest, to match the £100,000.

This may mean that you have a cash balance pot of around £86,000 today and the scheme offer you a transfer value of £74,000. In this example, the scheme have worked out that the cash balance going up by 3% a year for inflation, and the transfer value going up by 6% investment returns per year.

The transfer value offered will depend on the actuaries assumptions for inflation and investment returns.

For transferring, what you are hoping for is a bigger investment return on a smaller pot, that will eventually catch up and over take the inflation increasing notional pot. The nearer you are to retirement the smaller the difference between the cash balance pot and transfer value are likely to be, but of course over the short term there is less time for investment growth.

The counter to that is, the longer away you are from retirement, the smaller the pot, but the longer the investment growth.

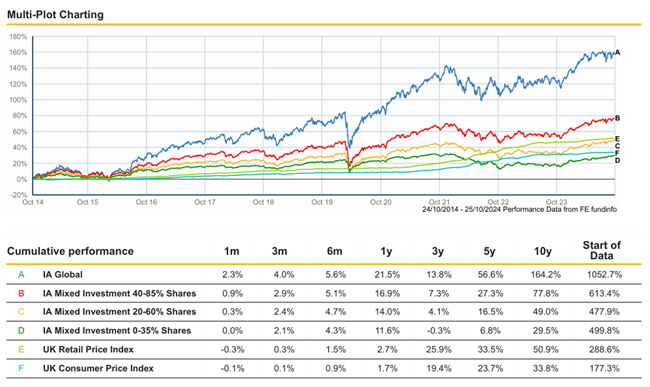

The chart below shows how investment growth (for certain investments) has gone up by more than inflation, over a 10 year period. Since the start of data, investments have beaten inflation.

Some companies that have a Cash Balance Pension

GlaxoSmithKline Wellcome Plan

Barclays Afterwork

AstraZeneca Pension Plan

Towers Perrin UK

Morrisons Retirement Savings Plan

Some schemes will also have conversion rates attached to the cash balance amount. This may mean they offer

If you want to discuss your pension, want advice, have a question, or just want to have a chat about it with a UK Qualified Independent Financial Adviser, then call us now on 01793 686393 or contact us online.